7 Important Accounting Concepts Your SMB Clients Need to Know

Updated on November 1, 2025 | 9 min. read

Do your clients have the knowledge they need to succeed? Cover these basic accounting concepts to strengthen their financial health—and your client relationships.

As an accounting professional, you’ve got a solid grasp of the accounting concepts that are vital to making informed financial decisions. But your small- and medium-sized business clients might need help.

You can’t be there to guide them through every business decision. But you can guide them through some important accounting principles up front in a clear, jargon-free way. Taking the time to explain these fundamentals lays the groundwork for long-term financial success for your client and positions you as a trusted advisor.

Here, we’ll break down accounting concepts small business owners get wrong, with some tips for explaining them in simple terms to your clients.

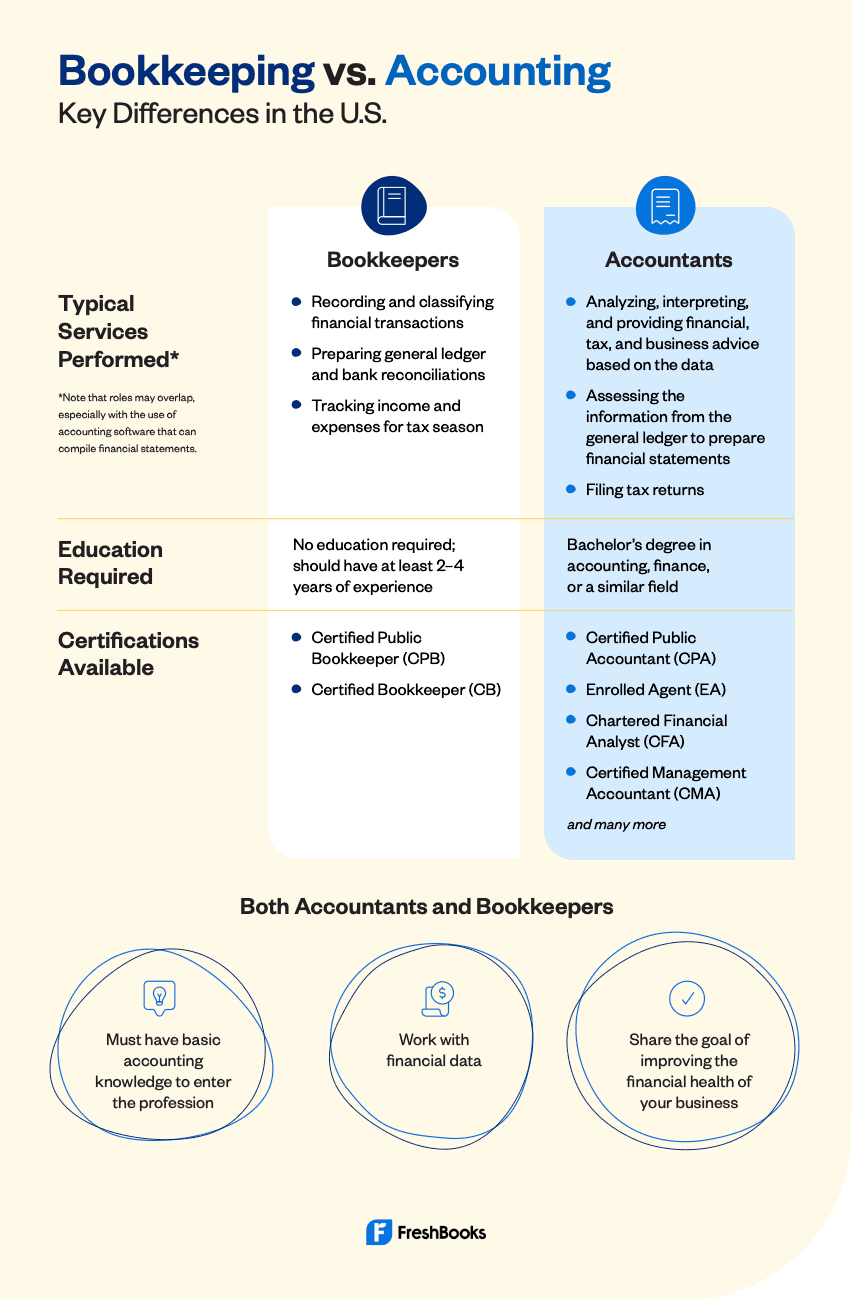

1. Bookkeeper vs. Accountant

When small business owners first set out to find an accounting professional, they might assume they need a CPA or an accountant rather than “just” a bookkeeper. Or they might be completely at a loss when it comes to which type of professional they need.

Some confusion is understandable because the roles and responsibilities aren’t always clearly defined. An accountant and bookkeeper may offer many of the same services. Finding the right accounting professional depends on a business owner’s unique needs and circumstances.

“The first thing I do to help clients understand which professional to choose, is to ask questions about their business and what they feel they need help with,” says Nayo Carter-Gray of 1st Step Accounting.

“Each role and license is a bit different, but we all work in tangent to ensure that the client’s needs will be met.”

Break It Down for Clients

First, encourage your clients to focus on the accounting professional’s experience and services rather than looking for the letters after their names.

Megan Justice, EA, LTC, at Crayon Advisory, takes a personalized, client-centric approach. “I focus on the client’s needs and connect them accordingly, matching their needs to the personality and capacity of the professional.”

“I filter through what the client needs and wants and what I know about the client as a human to make the best recommendation.”

You might share some high-level guidelines with your clients. For instance:

- If you need… day-to-day bookkeeping tasks like recording transactions, preparing financial statements, and ongoing support

👉 Consider hiring a bookkeeper - If you need… in-depth guidance on financial health improvements and analysis of business financial statements

👉 Consider working with an accountant - If you need… tax representation and/or audited financial statements for potential investors or lenders

👉 Hire a CPA—a certified public accountant in the U.S. or a chartered professional accountant in Canada (CPAs have passed the rigorous CPA exam and met specific educational and work experience requirements) - If you need… tax compliance, tax advice, and tax preparation assistance

👉 Consider a tax professional, or choose an enrolled agent for tax representation before the IRS (EAs are U.S. tax professionals who have demonstrated expertise in federal taxation and are licensed by the IRS)

This chart might help them understand some basic differences between bookkeeping and accounting.

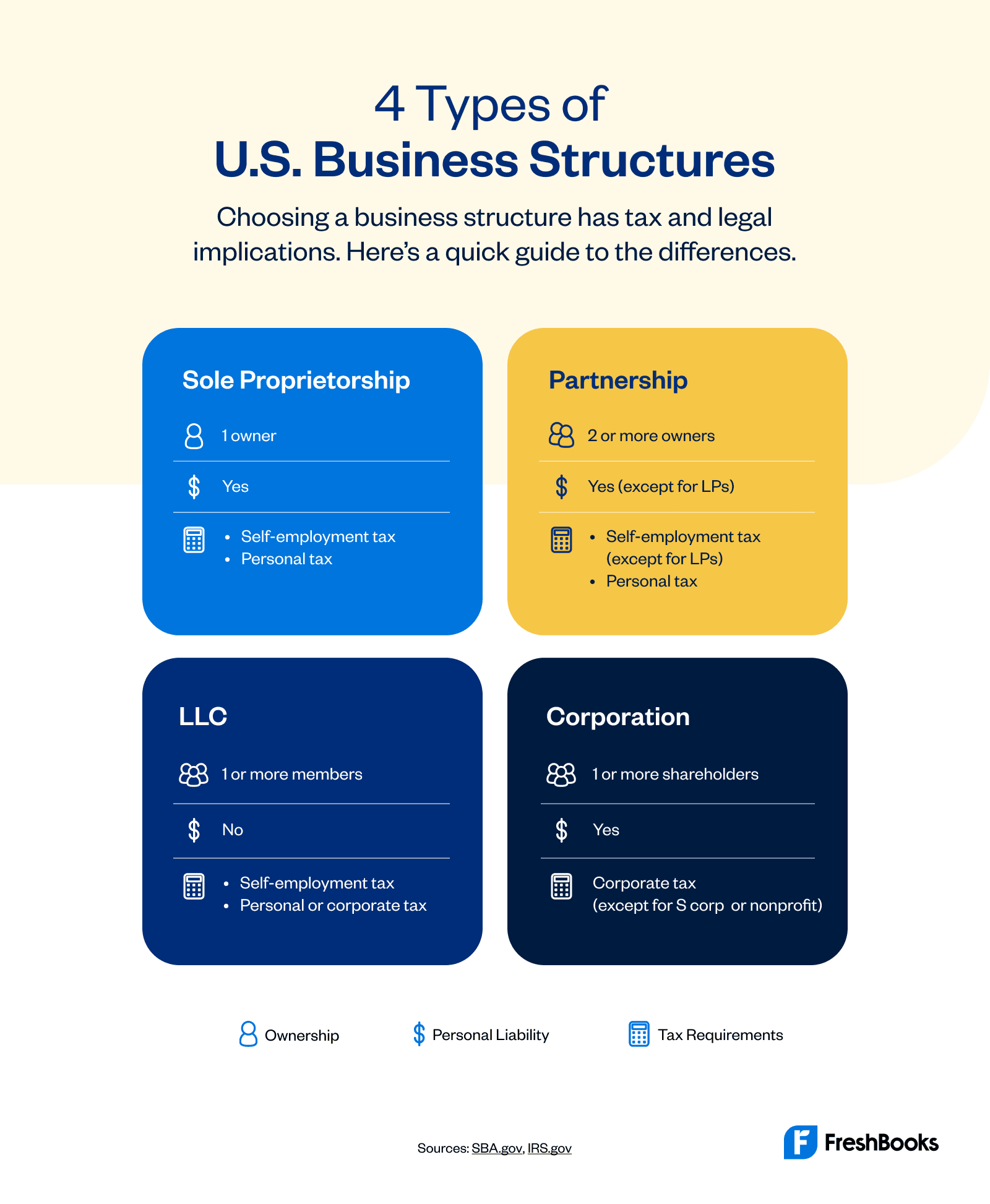

2. Business Entity Concept

Understanding the different business structures can be confusing, especially with so many options available. Each business entity has its unique advantages and disadvantages, including different tax implications that your clients may not fully grasp.

It’s important to guide them through the options if they’re starting out or if you’re advising a change to their business entity.

Break It Down for Clients

Review some business structure basics with clients:

Sole proprietorships are the simplest structure, perfect for small businesses operated by a single owner. It offers a straightforward way to report income and expenses on their tax return.

Partnerships are suitable for businesses with multiple owners who want to share profits, losses, and liabilities. They offer flexibility in management and structure but may have more complex tax requirements.

Limited liability companies (LLCs) provide liability protection and tax flexibility, so they’re a good choice for businesses with higher risk of legal issues.

Corporations are for businesses that want to establish a separate legal entity and provide liability protection for owners. C corps are best for larger businesses with shareholders, while S corps are for smaller businesses with limited shareholders looking to avoid double taxation.

3. Accounting Periods

Choosing an accounting period is a fundamental decision for business owners and can greatly impact financial reporting and taxes. The accounting period concept isn’t hard to understand, but knowing which one to choose for your business and all the implications of that decision can be.

Break It Down for Clients

Here’s how to explain accounting periods:

An accounting period is a specific time frame, such as a month, quarter, or year, in which a business records and reports its financial transactions. Think of it like taking a snapshot of the business’s financial performance during that period.

This is the period you will use on your company’s financial statements to compare financial data over time and follow trends in performance.

What’s the best accounting period? It depends on your business needs and preferences.

For example, if your business has seasonal income, you may use quarterly accounting periods for estimated tax payments to avoid overpaying or underpaying taxes. This way, your tax payments will match the income you earned and the expenses you incurred during each period.

On the other hand, if your business has a high volume of day-to-day transactions, monthly accounting periods may be better to ensure accurate and up-to-date financial information.

4. Cash vs. Accrual Accounting Method

Your clients might be scratching their heads over the difference between cash and accrual accounting. And who can blame them? It’s not exactly the most exciting topic out there.

But understanding which accounting method to use can really impact how they report their finances and how much they owe in taxes. So, it’s worth taking the time to break it down for them in a way that makes sense.

Break It Down for Clients

Here’s how Andrea MacDonald, CPA, from Pro Tax & Accounting, tackles this tricky subject with clients: “We start by explaining that it affects 2 areas of their business finances: Accounting and taxes.”

Her team doesn’t get too far into the weeds. “We ask our clients to trust us to choose the best method for them,” she says. “For small businesses, which is the only kind we work with, cash is typically the best method, at least for tax purposes.”

If your client wants a little more insight into accounting methods, you can help them weigh the pros and cons by giving them a brief 101, like this:

Cash-basis accounting is straightforward: Income is recorded when cash is received, and expenses are recorded when cash is paid. It provides a clear picture of the business’s cash flows but may not accurately reflect its financial performance.

Accrual-basis accounting recognizes income when earned and expenses when incurred, even if cash hasn’t been exchanged yet. This method considers all financial transactions and uses double-entry accounting to balance the books.

5. How to Read Financial Statements

Even when your clients have access to easy-to-use accounting software with automatically generated reports, they might find it hard to make sense of basic financial statements like their profit and loss statement (P&L) and balance sheets.

If your client doesn’t understand how to read and interpret these basic financial statements, they won’t have the knowledge they need to make smart decisions and plan for the future.

Break It Down for Clients

Financial statements show how a business is doing financially. They’re like a roadmap showing you where your business has been and where it’s headed.

Two of the most important financial statements to focus on are a company’s balance sheet and profit-and-loss statement (or P&L—also called an income statement).

The profit and loss statement shows your revenues, expenses, and net business income over a specific period. It helps you determine your business’s profitability and identify opportunities to cut costs or boost revenue.

The balance sheet summarizes your business’s financial position at a single point in time. It outlines a business’s assets, liabilities, and owner’s equity, so you know whether assets are enough to cover your liabilities and equity.

Check out this extensive guide for more information on how to help your clients read financial statements and their key metrics.

6. Difference Between Revenue, Profit, and Cash Flow

“Most clients do not understand how the profit that shows up on their tax returns can be higher than the cash sitting in the bank,” Andrea MacDonald points out.

That indicates they’re not grasping the relationship between revenue, profit, and cash flow. And without that understanding, a business owner may not know if their business is financially healthy.

To help clients bridge this gap, Andrea gets hands-on and creates a simplified cash flow statement for them. “The statement starts with revenue at the top, profit in the middle, and cash flow at the bottom,” she explains.

Break It Down for Clients

Here’s a simple way to explain it:

Revenue is the total amount of money you earn from selling your products or services.

Profit (or net profit) is the amount of money you have left over after deducting your expenses from your revenue.

Cash flow is the amount of cash moving in and out of your business, including both revenue and expenses.

You can also use a hands-on approach, like Andrea’s, by guiding them through a simple reconciliation of revenue and cash flow. Doing so will give them insights into how these metrics are interconnected and help them better understand their business finances.

7. Personal vs. Business Expenses

Small business owners sometimes end up using their personal funds to cover business costs. Sole proprietors, in particular, might not see the problem with combining business and personal finances. But mixing business and personal financial transactions puts business owners at risk and adds complexity at tax time.

Making the risks clear with your clients upfront and advising them on how to keep personal and business transactions separate will save many headaches down the line.

Break It Down for Clients

Your clients likely know the difference between business and personal expenses:

Personal expenses are for non-business purposes, such as groceries or entertainment.

Business expenses are expenses related to conducting business; these might include supplies, rent, or employee salaries.

Despite understanding this principle, clients still may not be recording financial transactions that way. In some cases, they aren’t fully aware of the risks of “piercing the corporate veil“—not to mention the extra time and cost to untangle each financial transaction for tax documentation.

Step 1 is to inform them of those pitfalls. Then, encourage them to open a business bank account and apply for a business credit card—and use them only for business transactions.

It’s All About Client Relationships

As an accounting professional, you have the power to help your small business clients achieve big financial success. You can empower them to make better financial decisions by guiding them through some key accounting concepts. It will benefit your clients but deepen your relationships with them, too—positioning you as a trusted financial advisor and contributing to the growth of your own business.